The Best Free Retirement Calculators in Canada [Updated]

How much money will you be able to spend in retirement? It sounds like a simple question, but it can be difficult to figure out. Canadians have to piece together retirement income from multiple different sources. These income streams may start at different times, be variable from year to year, and they might erode over time due to inflation.

There are many free retirement planning tools online, but you don't want to rely on faulty calculations. I tested 18 free retirement calculators to find out which, if any, can be reliably used to forecast income. In this article, I'll review the best and the worst, as well as common pitfalls to watch out for.

[2024 Update]

There is a new addition to the list of free retirement calculators this year. Investment company Steadyhand has provided a tool that earned a place as one of the three best free calculators.

Also, after briefly disappearing, Mawer's calculator has returned with some revisions. One of the changes is for the worse, but it still maintains its spot as one of the top three.

Retirement Planning Challenges

Before getting to the reviews, I want to touch on a few points about creating retirement projections. These tools are almost too easy to use. Being able to plug in numbers and get a plausible-looking result can hide errors.

There are a few things that have to be done correctly to get good results:

Understand each data entry point: You need to know exactly what each term means and how the data entry affects the output. This is not always as simple as it seems. While testing, I was constantly switching between data entry, the results page, and the assumptions disclaimer to make sure I understood what was going on.

Use good assumptions: Small changes in the assumptions used for investment returns and life expectancy can make a big difference in the results.

Many of the tools will have default settings, but they may not be appropriate for your situation. Default settings are powerful because if people don't know what to use, they're unlikely to change them. For example, I was disappointed to see the federal government calculator use average life expectancy as the default. The problem is that about half of Canadians will live longer than average.

Use good data: Trying to figure out how much income to expect from CPP and pensions can take some work. It is critical to get these amounts right however since they will form the foundation of your retirement income.

It's also important to know if your pension comes with annual inflation increases or not. Many don’t, but even the pensions with it will only have partial indexing.

Common Shortcomings

As a Certified Financial Planner®, I've created hundreds of retirement plans. Every financial calculator has strengths and weaknesses, including the professional options. A knowledgeable financial planner will be aware of these weaknesses and work around them.

Here are some common flaws I saw when reviewing these tools:

No control for CPP/OAS

No control for investment returns

Grouping RRSP/TFSA into one pot

No settings to stay within RRSP/TFSA contribution limits

Gross income target instead of net after-tax

Pension assumed to increase with inflation

No ability to indicate areas for improvement

Reports with little/no detail

Gross vs Net Income

The only item on the list above that isn't a serious issue is using a gross income target. Most people want to know how much they can spend in retirement, so net income would be more useful. To find the net value, you'll need to take the gross amount and enter it into a tax calculator.

A related problem is using the rule of thumb of needing 70% of your gross income in retirement. Each person's situation can vary so much that this estimate isn't very useful. Knowing your actual spending needs will help you really get the most out of these tools.

Detailed Reports

While many people would like a simple answer from a calculator, the lack of detailed reports is a big shortcoming for many of these tools. If you're relying on these calculations to decide when to quit, then you want to make sure that the numbers are correct. Without limited reports, there often isn't enough information to verify the results.

Testing Parameters

To compare all of the calculators, I created Bob, a fictional Canadian from Ontario:

Male Age 55

$100,000 employment income

Retire at 60

Life expectancy 94

$10,000 pension

$10,000 CPP at 65

Full OAS

$500,000 RRSP

$50,000 TFSA

These free calculators can barely handle a single person, so I wouldn't trust them for couples. Optimizing retirement income for a couple who are likely to be different ages, retiring at different times, and have different levels of income simply adds too much complexity for these free tools to handle.

The 3 Worst Retirement Calculators

When reviewing these free tools, I asked myself if I would be able to use them to help clients. The answer for each of these is a clear "No". Let's look at why:

Wealthsimple

Cons

RRSP and TFSA grouped together

Average CPP and Max OAS. Can't change

Very conservative net RoR in retirement of 2.77%. Can't change.

Very limited report/output

Unclear if other income is adjusted to inflation

I was able to include Bob's pension, but I couldn't tell if this amount would increase with inflation or not. Annual pension cost-of-living adjustments (COLA) make a HUGE difference over 30+ years. With just the one summary graph it was impossible to figure this out.

There is also a field to enter province of residence, but it doesn’t seem to do anything at all.

Sun Life

Cons

Low CPP and OAS. Can't change

Old data for OAS (2016) and tax (2021)

Average tax rate across all provinces?!

Very limited report/output

I like that they tried to calculate net income, but they went halfway by trying to use some weird set of averaged marginal tax brackets. Each province has different thresholds for their income brackets, so creating an average isn’t very useful.

Using old data for OAS shows that they don't care enough to keep it up to date. But I wouldn't have known this if I didn't check the assumptions section. Make sure you understand all the assumptions of any tool you use!

TD

Cons

Fixed investment returns. 5% pre-retirement and 2% afterwards.

Inflation fixed at 2%

Only 3 options for gross income target: 60/70/80%

No ability to check year-by-year calculations

Average CPP (2017) and Max OAS (2017?). Can't change

More of the same: lack of control and limited output. No way to really evaluate the results of this calculator due to the lack of details.

The 3 Best Retirement Calculators

Now let's look at the best of the free tools.

Disclaimer: I can't fully endorse any of these tools. Since I can't see "under the hood", there could be issues that I'm not aware of. But Bob's results with these three came reasonably close to my professional planning software.

Desjardins

Pros

Reasonable defaults for returns and life expectancy, with a custom option

Can adjust and defer CPP and OAS

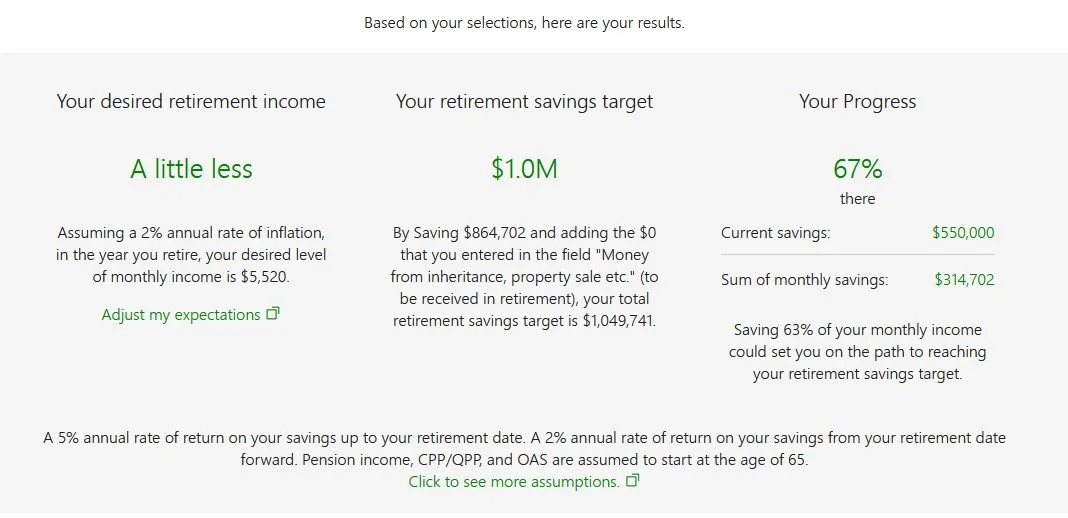

Detailed income breakdown on the results page

Cons

Uses gross income target

The inflation rate is unclear

Pension assumed to have full COLA

This is a good example of having enough data in the output to be useful. I couldn't find inflation being listed anywhere, but I was able to work it out based on the change in value of the investments over time. Works out to inflation of 2.1%

For those with a defined-benefit pension, be aware that this tool assumes a pension reduction at age 65. Not all pensions have this feature, so it's important to understand how yours works and to adjust accordingly.

There is an option to choose Ontario or Quebec as the province of residence, but since this tool uses gross income, I haven't been able to work out what changes.

Mawer

Pros

After-tax spending target

Can include future lump sum income/expenses

Extensive list of assumptions helps to understand how the tool works

Cons

Age 90 life expectancy with no option to change

Need to manually enter OAS

Limited investment return options, with minimum being 4.5%

This was the only tool to make a serious effort to calculate after-tax spending. Unfortunately, there isn't enough info to verify the accuracy of the calculations.

I also found it strange that they chose to leave out OAS by default. Some people could forget to include it. The input for other retirement income is also fully adjusted for inflation, so this might not be a good choice if you have a lot of pension income.

[2024 Update]

The Mawer calculator recently disappeared for a few weeks but is now up and working again. They updated the tax calculations which is noted in the assumptions tab. I’m glad to see that they’re maintaining their tool instead of letting it grow increasingly out-of-date (Sun Life).

They also changed the investment rate of return options, which I’m less pleased with. Previously, their options for returns ranged from 3.3% to 6.5%, but they increased the lowest illustrated return to 4.5%. This reduces the usefulness of the tool to show the range of possible outcomes in retirement.

Steadyhand

Pros

Ability to change income target at a later age.

Can control inflation rate for pensions and CPP/OAS

Can input a lump sum of additional savings (Sale of property, downsize, inheritance, etc...)

Cons

All investment accounts grouped together

Uses a gross income target

Lots of control may be potentially overwhelming.

New for 2024, we have a calculator provided by the investment company Steadyhand. This tool offers the highest level of control of the free options I’ve tried. I particularly like that a custom level of inflation indexing can be set on all of the income and savings inputs.

The downside is that this increased complexity might overwhelm some users. The greater control comes with a higher chance of making mistakes from misinterpreting the function of the inputs.

Nevertheless, this calculator is a nice addition for those who are comfortable making detailed adjustments to their retirement estimates.

Others Tools

Here is a list of the other free retirement calculators I looked at. They generally have at least a few of the common shortcomings discussed. If you know of others, please reach out to let me know.

Government of Canada

PERC

CIBC

MD

Fidelity

Raymond James

Get Smarter About Money

Scotia

Edward Jones

Canada Life

Creating a Retirement Plan

Finally, these tools create financial projections and they do not replace the work of a financial planner. A qualified financial planner can also help with:

Cash flow and debt management

RRSP drawdown strategies

Risk management

Tax planning

Estate planning

If you're considering professional help, it can be useful to know how to choose a retirement financial advisor who understands your specific needs and can guide you through these decisions.

If you’re feeling overwhelmed by all the work needed to create a plan, you can book a free introductory meeting with me.